By Peggy Creveling, CFA and

Chad Creveling, CFA

2nd May, 2023.

From time to time we are asked questions like, “Is USD 2 million enough for an expat to retire at 40 in Bangkok?” It’s a sensible question to ask—most of us aren’t likely to want to work longer than we have to, and $2 million in U.S. dollars is a sizeable amount to have set aside for retirement, especially if you’re an expat considering retiring in a relatively low-cost city such as Bangkok. But although USD 2 million is a lot, is it enough if you retire at the relatively young age of 40, with hopefully more than 50 years of retirement ahead of you? The answer is not the same for every expat. For those millionaires living overseas who are wondering if they have saved enough to retire, we provide some considerations to help you in your financial decision-making.

Factors You Need To Consider

To know whether you’re likely to have enough to retire, you need to factor in more than simply how much money you’ve saved. You also need to ask yourself:

1.How much will your intended lifestyle cost (including housing, food, clothing, appliances and furnishings, transportation, entertainment, medical, insurance, travel, and gifts)?

2.How do you expect your costs will inflate over time?

3.How are your savings invested, and are you hedged for currency risk?

4.What real rates of return might you expect, and how much risk is there to those rates of return?

5.What taxes and fees are applied to your investment earnings?

6.How long are you likely to live?

7.What could go wrong with your plans?

Assumptions

To run some scenarios, consider the case of Jack, a 40-year-old expat planning to retire in Thailand on USD 2 million (THB 68 million). Jack uses the following assumptions to consider if USD 2 million is enough for him to retire.

1.All lifestyle costs: USD 60,000 per year (c. THB 2 million per year or THB 170,000 per month), including all expenses: food, clothing, housing, appliances and furnishings, transportation, entertainment, travel, medical, insurance, gifting, etc.

2.Expected inflation of his expenses: Averaging about 3.87% per year in THB

3.How savings are invested: Jack wants to minimize risk and does not trust the stock market, so he plans to hold his savings on fixed deposit earning interest. Currently, he is receiving 4.43% pretax on interest (3.76% after tax). He expects that he will be able to earn a higher rate of return on fixed deposit in the future, about 5.0% pretax or 4.3% after tax.

4.What real rates of return are expected: The after-tax bank deposit rate is currently slightly less than the current rate of inflation, so it represents a negative real rate of return. However, Jack believes this is an unusual situation and expects it to change in the future. He factors in long-term fixed deposit rates to be slightly higher than inflation.

5.Taxes and fees applied to investment earnings: A 15% withholding rate on interest received

6.Life expectancy: 92 years (although 30% of healthy 40-year-old men might live past age 92)

7.What could go wrong: In 52 years of retirement a lot could go wrong, including (but not limited to) overall higher-than-expected living costs (especially medical expenses), higher inflation rates over time, other unexpected costs, bank failure, lower real rates of return, increased tax rates, etc.

Initial Results

Currently, even a simple spreadsheet analysis using Jack’s assumed long-term average annual rate of return (5.0% per year pretax, 4.3% after tax shows that he will very likely run out of money in the future:

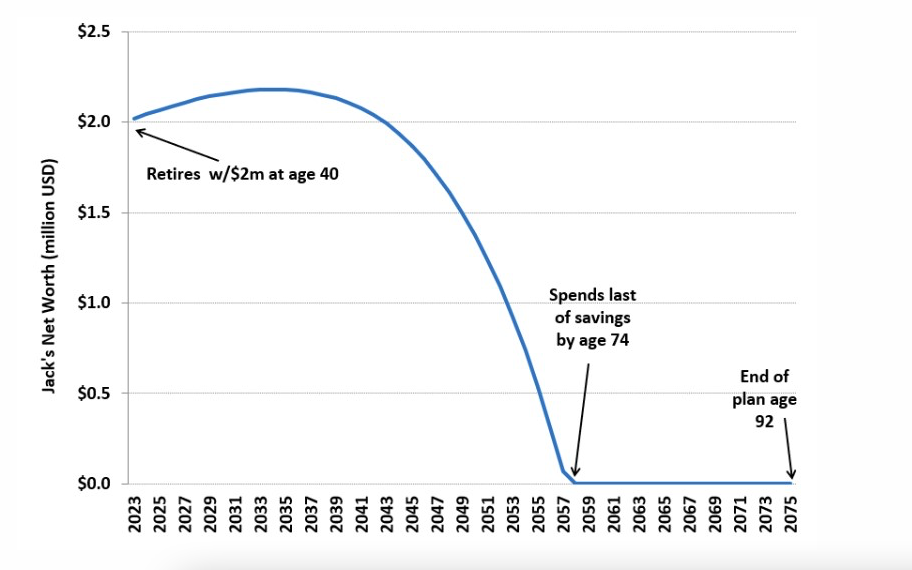

Jack’s Net Worth in Retirement

At first, Jack’s net worth rises. However, at some point in the future, the growth in his annual spending will be greater in absolute terms than the growth in his investment portfolio, and his savings will be spent down quickly. Jack could be penniless by age 74.

In the above graph, note that rather deceptively in the early years, Jack’s net worth rises annually, since at first his initial after-tax portfolio earnings exceed his initial retirement spending. However, since he is also reducing his portfolio each year because of his annual spending, at some point his annual spending increases at a greater absolute amount than does his reduced portfolio (since he’s spent a portion of it). The table below illustrates the difference between the early years, the peak years, and the plummet.

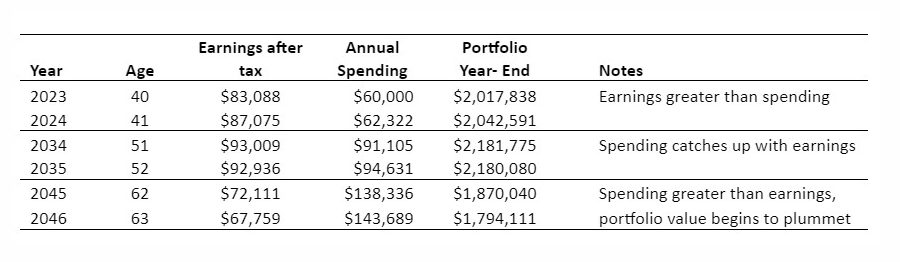

Jack’s Earnings Versus Spending Over Time

As shown in the table above, in some future year—in this case, 11 years from now—Jack’s portfolio peaks in size and then begins to plummet in value. He is penniless by age 74. This could be an optimistic outcome; we’re assuming a positive real rate of return on his fixed deposits, which is not always the case for fixed-income investments. Jack would be penniless faster if real rates of return are negative for a period.

Improving Jack’s Chances Of Not Running Out Of Money

One thing Jack might do is diversify some of his savings into asset classes besides just fixed deposits. Few people are able to save enough to retire on a portfolio that is invested entirely in either cash or cash-like investments such as bank short-term fixed deposits. This is especially the case if the investment horizon (retirement period) is as long as Jack’s, who could spend 50 years or more in retirement. The expected long-term real rate (after inflation) of return of cash or fixed deposits is simply too low. The earnings, even on millions of dollars, may not be enough to cover living expenses and inflation.

Therefore, Jack could seek to increase his expected long-term real rate of return by including some higher expected return investments in his portfolio, such as global equities (stocks), real estate, and specialty bonds. If properly diversified, these asset classes can provide a hedge against inflation and thereby boost Jack’s long-term expected real rate of return. While adding these asset classes to the mix will also increase the portfolio’s short-term volatility (risk), it will increase his chances of not outliving his money. Putting up with short-term volatility is the price that must be paid in order to get a chance at earning a better long-term return. However, he may still wish to keep a reasonable portion of his savings in Thai baht fixed income.

What Else Can Jack Do?

While diversifying his portfolio will help improve Jack’s chances of not outliving his savings, it may not be enough. Even if a simple Excel spreadsheet analysis indicates that with a higher expected rate of return his savings could last for 50 years, Jack still should consider what could go wrong with his assumptions. For example, a globally diversified portfolio may not do as well as expected. His costs could be higher than anticipated for any number of reasons, including higher than- expected inflation, currency depreciation, failing health or disaster, or even if he simply wishes to provide financial help to someone near to him. Jack might also live longer than he expects.

With a very long potential retirement period (in this case 50 years or more), planning for a number of different scenarios— including some worst-case ones—only makes sense. If the numbers do not add up, Jack could consider either reducing his spending now or perhaps working part-time for a period. In 10 or 15 years he may be very glad he did.

Summary

While USD 2 million is a lot to have saved for retirement, due to higher cost of living it does not go as far as it used to—even for expats seeking to retire in a relatively low-cost country such as Thailand. Going forward, inflation will continue to whittle away spending power. This is especially the case for relatively young expats who may have many years of retirement ahead. To lessen the chance of running out of money in retirement, those seeking to retire on their savings should consider all aspects of their financial situation, considering not only how much they have saved, but also their actual spending habits, inflation, currency risk, how they are investing their savings, and finally what could go wrong. Depending on the situation, keeping all your savings on fixed deposit may not make sense. Holding a more diversified portfolio, seeking to cut spending, or working part-time could all go a long way to making your retirement savings last.

This article is a revised and updated version of an article that originally appeared on www.crevelingandcreveling.com.

https://www.crevelingandcreveling.com/blog/retire-at-40