I know nothing about money and financial stuff but weren't shady and underregulated derivatives consisting mostly of bad mortgages the main reason for the 2008 financial collapse?scobienz wrote: ↑Thu Jun 25, 2020 1:27 pmThey’re used but it is what the industry calls ‘one directional use’. In other words they are used to reduce risk (my example of using shorts in a falling market for example) and NOT for growth. The most common instruments used are interest rate and inflation swaps, for obvious reasons.

Their use is marginal and well regulated.

The Future of the US Dollar

None but ourselves can free our mind.

-

kungfufighter

- OneTrickPony

- Reactions: 64

- Posts: 1640

- Joined: Tue Aug 20, 2019 12:48 pm

Credit Default Swaps

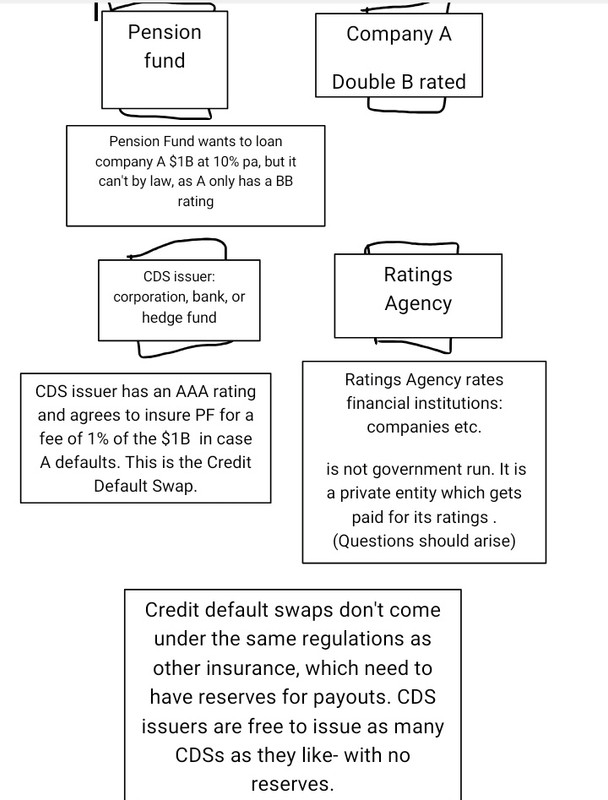

Now consider what happens if there are too many CDSs issued and people start defaulting. Remember, the CDS is a type of insurance that is unregulated and, therefore, doesn't need to have any reserves to back it.

For a good visualisation take this

and times it by this

Now name the CDS issuer as AIG, and the ratings agency as Moody's.

Credit Default Swaps, as Warren Buffet says, are financial weapons of mass destruction.

And they've been used with everybody's pensions.

Now consider what happens if there are too many CDSs issued and people start defaulting. Remember, the CDS is a type of insurance that is unregulated and, therefore, doesn't need to have any reserves to back it.

For a good visualisation take this

and times it by this

Now name the CDS issuer as AIG, and the ratings agency as Moody's.

Credit Default Swaps, as Warren Buffet says, are financial weapons of mass destruction.

And they've been used with everybody's pensions.

Up the workers!

Pension funds don’t lend money kff. I think you’re confusing pension funds with investment management companies who may manage pension funds (which are managed by a board of trustees) as part of their overall activities.

A bad investment by, say, AIG as part of its general commercial activities has no impact at all on any pension fund they manage. AIG, as the fund manager, could even go bankrupt and still the pension fund is unaffected, except insofar as its board of trustees would need to appoint a new fund manager. It would impact the fund value one penny.

A bad investment by, say, AIG as part of its general commercial activities has no impact at all on any pension fund they manage. AIG, as the fund manager, could even go bankrupt and still the pension fund is unaffected, except insofar as its board of trustees would need to appoint a new fund manager. It would impact the fund value one penny.

That is not true. I can name numerous pension funds that were altered, subsidized and even fell flat. You mention AIG. How about Elron?

Bankruptcy, and pensions do not mix. They also lose their dividends and anything else.

Scobienz, you do not work with any of this, do you?

Bankruptcy, and pensions do not mix. They also lose their dividends and anything else.

Scobienz, you do not work with any of this, do you?

I should clarify. I’m talking about private pension plans, not company schemes like Enron (I assume you mean that) where the liability for the pension remains on the employers’ balance sheet.Scobienz Tutor wrote: ↑Fri Jun 26, 2020 1:06 pmThat is not true. I can name numerous pension funds that were altered, subsidized and even fell flat. You mention AIG. How about Elron?

Bankruptcy, and pensions do not mix. They also lose their dividends and anything else.

Scobienz, you do not work with any of this, do you?

The huge liability of these company final salary schemes and the risk to the holder due to corporate failure, is why they have been largely eliminated from the private sector in recent years, and replaced by DC pensions.

Liability does not remain on the employers' balance sheet if it effects thier backruptcy and ultimately never ends well for the pensioners in living history.

Give me an example. AIG? HSBC? Let's try that, for example. How is that working out for them. Do you think they lock it up in a bank account or vault? Tell that to the pensioners who have lost everything in the UK!

Give me an example. AIG? HSBC? Let's try that, for example. How is that working out for them. Do you think they lock it up in a bank account or vault? Tell that to the pensioners who have lost everything in the UK!

DC pensions?? Largely been eliminated? This is certainly not your area of expertise.

-

kungfufighter

- OneTrickPony

- Reactions: 64

- Posts: 1640

- Joined: Tue Aug 20, 2019 12:48 pm

How did people lose their pensions in the 2008 global financial crisis?

Hmm, in simple and simplified terms : pension funds are company-sponsored (private) financial entities that invest money on behalf of their contributors - usually company employees - and provide income for employees of the company in retirement. Usually, when contributors reach a certain age, the available money can be pulled off the fund (mostly)free of government fees .That's - for our purpose - how a pension fund works, as opposed to a general purpose investment fund .

A lot of people have their retirement savings - deposited perhaps as a fraction of every paycheck - not in saving bank accounts but in these pension funds - the thinking being that through investing they get a higher rate of return ; and that is true in the long run - but the truth is also that while pension fund managers are very careful with keeping the risk level of their investment activity low, pension fund investing , like any investment, carries the risk of loss, especially in the short and medium term.

In particular, many pension funds across the world had in 2008 invested in stocks and derivatives based on the US real estate market, one of the - historically - most secure investment destinations. It could be argued that the amount of money invested by entities looking for a secure placement for their money - pension funds among them - and finding it in the US real estate market - was a contributing factor to the rise of the real estate bubble and its eventual collapse.

When that market collapsed, those investments lost a lot value - their market (sale) value went lower than their cost basis - the value they were bought at.

So if one wanted to retire in the 2008-2012 and planned to get money out of his pension fund, he suddenly had - for the 100 000 one had put in it, instead of the 400 000 that were available at the end of 2007, just 50 000 at the end. Some arbitrary values there to exemplify the point. That's loss.

Now, if one had time to wait, some of these investments partially recovered value so perhaps towards 2013 things were not looking as bleak anymore ( ). If one, on the other hand liquidated his fund holding at that low in the market, or the fund manager did - the loss became pretty much permanent.

). If one, on the other hand liquidated his fund holding at that low in the market, or the fund manager did - the loss became pretty much permanent.

Which leads us on to Collateralized Debt Obligations or CDOs and Mortgage Backed Securities...

Hmm, in simple and simplified terms : pension funds are company-sponsored (private) financial entities that invest money on behalf of their contributors - usually company employees - and provide income for employees of the company in retirement. Usually, when contributors reach a certain age, the available money can be pulled off the fund (mostly)free of government fees .That's - for our purpose - how a pension fund works, as opposed to a general purpose investment fund .

A lot of people have their retirement savings - deposited perhaps as a fraction of every paycheck - not in saving bank accounts but in these pension funds - the thinking being that through investing they get a higher rate of return ; and that is true in the long run - but the truth is also that while pension fund managers are very careful with keeping the risk level of their investment activity low, pension fund investing , like any investment, carries the risk of loss, especially in the short and medium term.

In particular, many pension funds across the world had in 2008 invested in stocks and derivatives based on the US real estate market, one of the - historically - most secure investment destinations. It could be argued that the amount of money invested by entities looking for a secure placement for their money - pension funds among them - and finding it in the US real estate market - was a contributing factor to the rise of the real estate bubble and its eventual collapse.

When that market collapsed, those investments lost a lot value - their market (sale) value went lower than their cost basis - the value they were bought at.

So if one wanted to retire in the 2008-2012 and planned to get money out of his pension fund, he suddenly had - for the 100 000 one had put in it, instead of the 400 000 that were available at the end of 2007, just 50 000 at the end. Some arbitrary values there to exemplify the point. That's loss.

Now, if one had time to wait, some of these investments partially recovered value so perhaps towards 2013 things were not looking as bleak anymore (

Which leads us on to Collateralized Debt Obligations or CDOs and Mortgage Backed Securities...

Up the workers!

And reading is clearly not yours. I did not say DC pensions have been eliminated. DB pensions have been virtually eliminated and replaced by DC.Scobienz Tutor wrote: ↑Fri Jun 26, 2020 1:31 pmDC pensions?? Largely been eliminated? This is certainly not your area of expertise.

kungfufighter wrote: ↑Fri Jun 26, 2020 1:36 pmHow did people lose their pensions in the 2008 global financial crisis?

Hmm, in simple and simplified terms : pension funds are company-sponsored (private) financial entities that invest money on behalf of their contributors - usually company employees - and provide income for employees of the company in retirement. Usually, when contributors reach a certain age, the available money can be pulled off the fund (mostly)free of government fees .That's - for our purpose - how a pension fund works, as opposed to a general purpose investment fund .

A lot of people have their retirement savings - deposited perhaps as a fraction of every paycheck - not in saving bank accounts but in these pension funds - the thinking being that through investing they get a higher rate of return ; and that is true in the long run - but the truth is also that while pension fund managers are very careful with keeping the risk level of their investment activity low, pension fund investing , like any investment, carries the risk of loss, especially in the short and medium term.

In particular, many pension funds across the world had in 2008 invested in stocks and derivatives based on the US real estate market, one of the - historically - most secure investment destinations. It could be argued that the amount of money invested by entities looking for a secure placement for their money - pension funds among them - and finding it in the US real estate market - was a contributing factor to the rise of the real estate bubble and its eventual collapse.

When that market collapsed, those investments lost a lot value - their market (sale) value went lower than their cost basis - the value they were bought at.

So if one wanted to retire in the 2008-2012 and planned to get money out of his pension fund, he suddenly had - for the 100 000 one had put in it, instead of the 400 000 that were available at the end of 2007, just 50 000 at the end. Some arbitrary values there to exemplify the point. That's loss.

Now, if one had time to wait, some of these investments partially recovered value so perhaps towards 2013 things were not looking as bleak anymore (

Which leads us on to Collateralized Debt Obligations or CDOs and Mortgage Backed Securities...

Of course the underlying assets in pensions go up and down. That is why most people adjust their asset mix as they get closer to retirement age, usually away from stocks to bonds or cash.

Exactly the same applies to every asset class, including bitcoin.

I’m still struggling to understand the point you’re using copy and paste to make.

Scobienz Tutor wrote: ↑Fri Jun 26, 2020 1:27 pmLiability does not remain on the employers' balance sheet if it effects thier backruptcy and ultimately never ends well for the pensioners in living history.

Give me an example. AIG? HSBC? Let's try that, for example. How is that working out for them. Do you think they lock it up in a bank account or vault? Tell that to the pensioners who have lost everything in the UK!

HSBC moved from a DB scheme (which keeps the liability on their balance sheet) to a D.C. scheme nearly 25 years ago. If HSBC went bust now, only the legacy DB members would be affected and of course there are fewer and fewer of them.

All their current employees since 96 have been on DC pensions, and so would be unaffected by the demise because this pot of money is NOT held by HSBC.

Company schemes like the old HSBC DB scheme are never your money. They remain the company’ money and you are basically relying on them to pay it forever. Who would take that risk?

A DC scheme on the other hand remains assigned to you all your life.

Just as an aside, this whole debate began when kff wrongly suggested that pensions had been derivitised and that we were suckers who were caught up in a bubble.

What’s the fastest growing asset class for derivatives right now? Well you guessed it. Cryptocurrencies like Bitcoin.

And why? So that fund managers can include crypto in their currency while using the derivitisation to manage the risk of an inherently volatile asset class.

https://uk.news.yahoo.com/bitcoin-deriv ... 28481.html

What’s the fastest growing asset class for derivatives right now? Well you guessed it. Cryptocurrencies like Bitcoin.

And why? So that fund managers can include crypto in their currency while using the derivitisation to manage the risk of an inherently volatile asset class.

https://uk.news.yahoo.com/bitcoin-deriv ... 28481.html

-

kungfufighter

- OneTrickPony

- Reactions: 64

- Posts: 1640

- Joined: Tue Aug 20, 2019 12:48 pm

It seems that a lot of people support the bail outs and fiscal monetary policy because at least they will save people's pensions. But is this true?

Traditional, most pension funds invest a large percentage in government bonds. But, at 0% interest, they are increasingly unable to balance their books.

What we see is that future liabilities increase because people get older, and at the same time future asset value does not increase because the interest is close to 0.

This means that pension funds face a funding ratio below 1, meaning they have to pay more future pensions than there is money to fund it with in the future, at least according to the calculation.

Regulators press pension funds to increase the funding ratio, and pension funds have only two options:

Increase inflow of money, the contributions people make prior to retirement

Decrease the outflow of money, in other words decrease future liabilities

The second option hits people close to retirement, the first those who are still building pension. The latter face that the amount “saved” decreased, the former face that they need to pay more for the same amount of pension of those who retired, a lower return on investment.

Many funds worked both ways to improve their funding ratios, increase contribution and lower liabilities.

Many people lost their savings in the 2008 crisis due to wrong investment, a huge amount of pension “virtually damped” because of the low interest rates to which future asset values are calculated.

Another large part of the problem, is pension funds also invest a large percentage in real estate which is in a huge over-inflated bubble waiting to pop.

All this means that pension funds are now looking at more creative ways to balance their books like investing in corporate bonds. With a super over inflated stock market and an estimated 25% of zombie companies, the whole arena is looking highly volatile.

So, maybe it's not such a good idea to bail out the banks and stock market, after all.

Blame The Fed For The Coming Pension Fund Crisis

Aug. 26, 2019 12:07 AM ETAGG, BIBL,

Most public and private pensions in the United States are underfunded, many severely so.

Back when interest rates floated in a historically normal range, there was not a serious issue of pension underfunding.

Ultra-low interest rates have pushed pensions into riskier assets such as corporate equities and bonds.

Pension demand for corporate bonds has facilitated a surge of debt-funded buybacks.

What happens when pensions are no longer able to keep up their massive procurement of corporate debt?

American pensions are in trouble.

https://seekingalpha.com/article/428782 ... und-crisis

Traditional, most pension funds invest a large percentage in government bonds. But, at 0% interest, they are increasingly unable to balance their books.

What we see is that future liabilities increase because people get older, and at the same time future asset value does not increase because the interest is close to 0.

This means that pension funds face a funding ratio below 1, meaning they have to pay more future pensions than there is money to fund it with in the future, at least according to the calculation.

Regulators press pension funds to increase the funding ratio, and pension funds have only two options:

Increase inflow of money, the contributions people make prior to retirement

Decrease the outflow of money, in other words decrease future liabilities

The second option hits people close to retirement, the first those who are still building pension. The latter face that the amount “saved” decreased, the former face that they need to pay more for the same amount of pension of those who retired, a lower return on investment.

Many funds worked both ways to improve their funding ratios, increase contribution and lower liabilities.

Many people lost their savings in the 2008 crisis due to wrong investment, a huge amount of pension “virtually damped” because of the low interest rates to which future asset values are calculated.

Another large part of the problem, is pension funds also invest a large percentage in real estate which is in a huge over-inflated bubble waiting to pop.

All this means that pension funds are now looking at more creative ways to balance their books like investing in corporate bonds. With a super over inflated stock market and an estimated 25% of zombie companies, the whole arena is looking highly volatile.

So, maybe it's not such a good idea to bail out the banks and stock market, after all.

Blame The Fed For The Coming Pension Fund Crisis

Aug. 26, 2019 12:07 AM ETAGG, BIBL,

Most public and private pensions in the United States are underfunded, many severely so.

Back when interest rates floated in a historically normal range, there was not a serious issue of pension underfunding.

Ultra-low interest rates have pushed pensions into riskier assets such as corporate equities and bonds.

Pension demand for corporate bonds has facilitated a surge of debt-funded buybacks.

What happens when pensions are no longer able to keep up their massive procurement of corporate debt?

American pensions are in trouble.

https://seekingalpha.com/article/428782 ... und-crisis

Up the workers!

-

kungfufighter

- OneTrickPony

- Reactions: 64

- Posts: 1640

- Joined: Tue Aug 20, 2019 12:48 pm

Yes, I'm not too sure about the overall implications of derivatives being used on Bitcoin, yet.scobienz wrote: ↑Fri Jun 26, 2020 7:29 pmJust as an aside, this whole debate began when kff wrongly suggested that pensions had been derivitised and that we were suckers who were caught up in a bubble.

What’s the fastest growing asset class for derivatives right now? Well you guessed it. Cryptocurrencies like Bitcoin.

And why? So that fund managers can include crypto in their currency while using the derivitisation to manage the risk of an inherently volatile asset class.

https://uk.news.yahoo.com/bitcoin-deriv ... 28481.html

It may encourage more people to see Bitcoin as a viable asset.

I think it would be the totally wrong reason to get into it though.

The real reason to get into Bitcoin is that people should be so livid at what a small group of people have been doing to enrich themselves, destabilise the world, and make everyone, including the middle classes, much much poorer, would be the right reason.

Up the workers!

-

- Similar Topics

- Replies

- Views

- Last post

-

-

Future of Pattaya - the options

by Expatissimo » Wed Sep 15, 2021 8:49 am » in Thailand, Vietnam, Myanmar and Lao forums - 0 Replies

- 1221 Views

-

Last post by Expatissimo

Wed Sep 15, 2021 8:49 am

-

-

-

Future of Xinjiang China Uyghur People

by marukai » Thu Nov 14, 2019 12:10 pm » in Cambodia Speakeasy - 16 Replies

- 5090 Views

-

Last post by Orichá

Thu Jan 02, 2020 12:46 am

-

-

- 29 Replies

- 1438 Views

-

Last post by MarkinAston

Tue Jun 20, 2023 7:25 am

-

-

Cambodia’s NagaWorld Casino Expansion Delayed, Company Ponders Future

by Bong Burgundy » Tue Jun 06, 2023 11:38 am » in Cambodia News - 3 Replies

- 470 Views

-

Last post by schlarry

Tue Jun 06, 2023 6:42 pm

-